|

Getting your Trinity Audio player ready...

|

Introduction: You Don’t Need Thousands to Start

When I first thought about investing, I had this misconception that I needed thousands of dollars sitting in my bank account before I could even think about putting my money to work. Looking back, I wish someone had told me earlier that you can absolutely begin your journey toward building wealth with just spare change and a willingness to learn.

The truth is: investing is not reserved for the wealthy—it is a long-term strategy that anyone can adopt to pursue their financial goals, whether that means:

- Saving for a down payment on a new house

- Funding your retirement

- Simply watching your money grow over time

⚠️ Important Disclaimer: Before you start, understand that investment products can lose value, are not bank guaranteed, not FDIC insured, not a deposit, and not insured by any federal government agency—so going in with realistic expectations is essential.

What is Investing and Why Does It Matter?

At its core, investing means putting your money into investment vehicles that have the potential for greater returns compared to a traditional savings account.

| Feature | Savings Account | Investing |

|---|---|---|

| Risk Level | Lower risk | Higher risk |

| Returns | Lower reward | Potentially greater returns |

| Access | Immediate access | Long-term commitment |

| Growth | Limited | Compound annual growth |

While a savings account gives you easier access to your funds for things like Deposit products offered by institutions like U.S. Bank National Association (Member FDIC), it typically offers lower risk with lower reward.

Investing, on the other hand, asks you to accept more risk in exchange for the possibility of seeing your investment dollars multiply over the years. This is not about getting rich overnight—it is about understanding that time is your greatest ally.

The Magic of Compound Growth

The power of compound growth is what I like to call the secret ingredient. When the return on your investment starts generating its own return, you experience compound annual growth.

Example: Watch how $1,000 grows:

- Year 1: $1,000 → $1,070 (7% return = $70)

- Year 2: $1,070 → $1,144.90 (7% return = $74.90, an extra $4.90)

- Over thousands of dollars and many years, these small gains add up to something remarkable

Fighting Inflation and Building Real Value

One of the biggest reasons I started taking investing seriously was learning about inflation. Inflation quietly erodes the value of the dollar in your wallet.

The Inflation Math

| Scenario | Rate | Result |

|---|---|---|

| Annual inflation rate | 3% | Your money needs to earn at least this much just to break even |

| Most savings accounts | ~0.5% | Cannot match inflation |

| S&P 500 historical average | 7% | Beats inflation significantly |

| Real return after inflation | 4% | Actual wealth growth |

So if your investments earn 7% on average, your real return after accounting for inflation ends up around 4%. This means your money is actually growing in terms of purchasing power, helping you afford those groceries and everyday needs without losing ground.

Understanding how inflation affects all areas of the economy and your investment returns is fundamental to making smart decisions, especially when economic developments and business developments shift the landscape.

Getting Your Financial House in Order First

Before diving into any investment options, I learned the hard way that your financial situation needs a solid foundation.

✅ Pre-Investment Checklist

Ask yourself these questions before you start investing:

- [ ] Do you have an emergency fund covering three to six months of living expenses?

- [ ] Have you tackled any high-interest debt like credit card debt or personal loans?

- [ ] If considering credit products, do you understand credit approval requirements?

- [ ] Do you have extra money left after paying your expenses each month?

If you answered “no” to any of these, focus there first.

Investing carries risks as well as potential rewards, and since it is a long-term strategy, you should only invest money you can live without. The possibility of loss or even principal loss is real, so your safety net must be in place first.

Crafting Your Personal Investment Strategy

Your investment strategy is essentially your roadmap. It defines:

- Your financial goals – What are you saving for?

- Your age and timeline – How long until you need the money?

- Your risk tolerance – How much volatility can you handle?

- Your preferred method – Working with a financial professional or going solo?

Age-Based Strategy Adjustment

When I was younger, I could afford to be more aggressive because my money had decades to recover from potential losses. As you get older and approach retirement, you may want to lower your risk and protect what you have built.

Your strategy should also account for diversification—spreading your money across various investment vehicles and asset classes to avoid putting all your eggs in one basket.

📝 Note: Diversification and asset allocation do not guarantee returns or protect against losses, but they can help manage risk.

Consider consulting a tax advisor or legal advisor for tax and legal advice specific to your situation, as tax ramifications vary based on your choices.

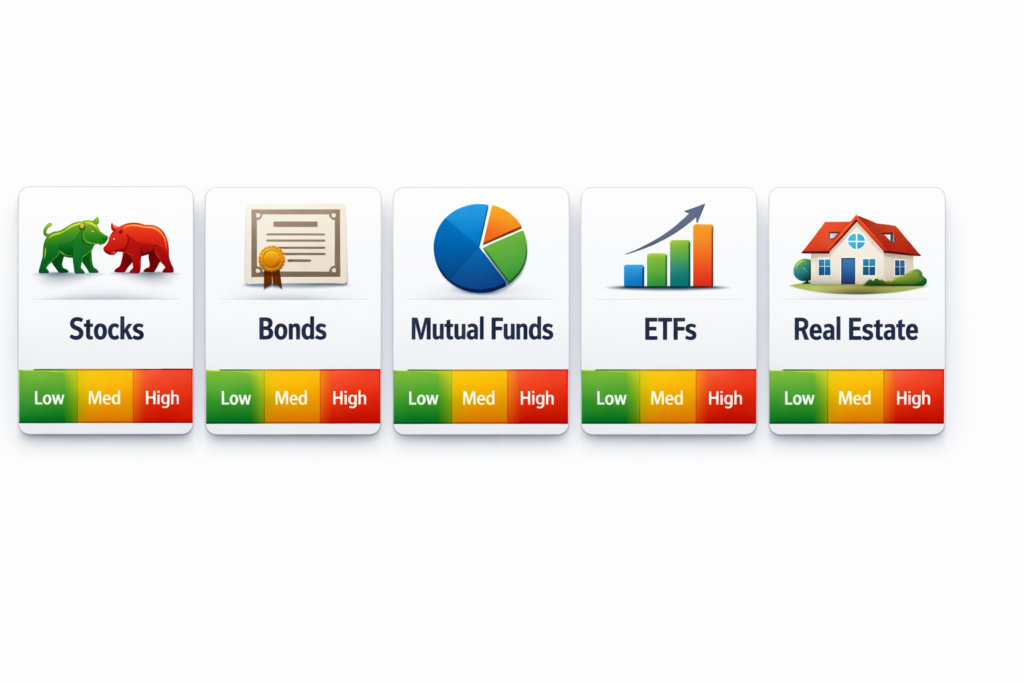

Understanding Different Investment Vehicles

There is a whole world of investment vehicles out there, and knowing your options helps you build a diversified portfolio.

Stocks (Equities)

Stocks represent a share of ownership in a company—these are also called equities or equity securities. They are subject to stock market fluctuations that occur in response to economic developments and business developments.

Bonds (Fixed Income)

Bonds are essentially a loan you make to an entity like a government or corporation. Types include:

- Corporate bonds

- High-yield bonds

- Municipal bonds

- Mortgage bonds

⚠️ Risk Disclosure: Investments in fixed income securities are subject to various risks, including changes in interest rates, credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, and other factors. Investment in fixed income securities typically decrease in value when interest rates rise, and this risk is usually greater for longer-term securities. Investments in lower-rated securities and non-rated securities present a greater risk of loss to principal than higher-rated options.

Mutual Funds

A mutual fund pools money from many investors to invest in securities, with types including:

- Equity funds

- Fixed-income or bond funds

- Money market funds

Mutual fund investing involves risk and principal loss is possible. Investing in certain funds involves special risks, such as those related to investments in small-capitalization stocks, mid-capitalization stocks, foreign securities, debt securities, and high-yield securities, as well as funds that focus their investments in a particular industry. Please refer to the fund prospectus for additional details.

Exchange-Traded Funds (ETFs)

An exchange-traded fund or ETF tracks a stock market index, a specific sector, or a commodity like natural gas or wheat.

Exchange-traded funds or ETFs are baskets of securities that are traded on an exchange like individual stocks at negotiated prices and are not individually redeemable. ETFs are designed to generally track a market index and shares may trade at a premium or a discount to the net asset value of the underlying securities.

Real Assets

Real assets are tangible investments in things like:

- Real estate

- Commodities

- Infrastructure

Each carries its own growth profile, risk level, and diversification considerations.

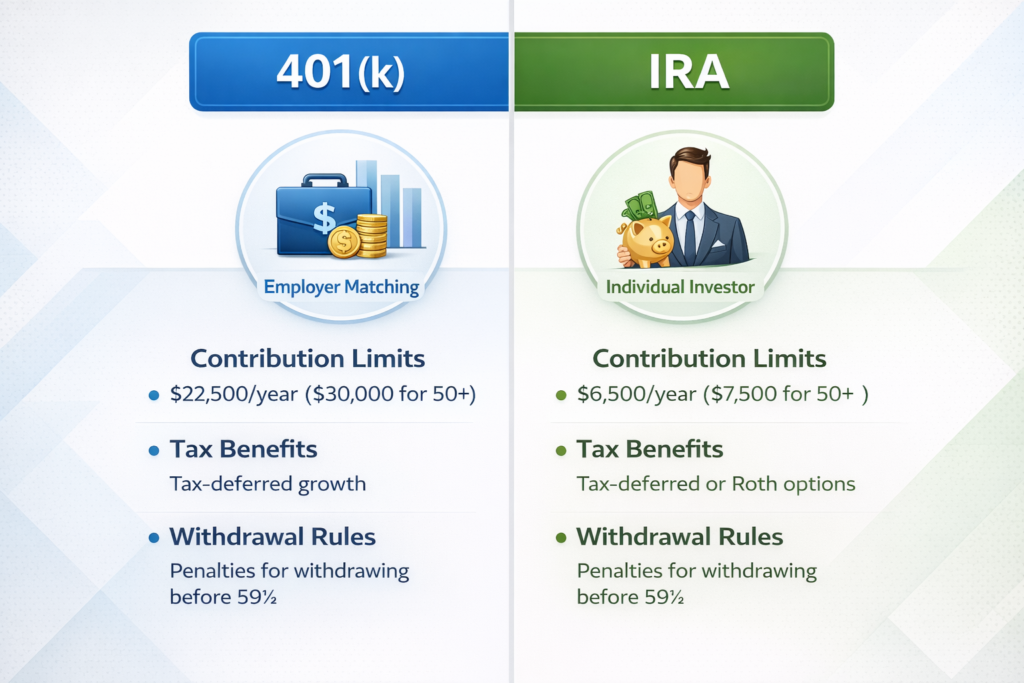

Choosing the Right Investment Accounts

Where you hold your investments matters for your taxes and overall investment goals.

Retirement Accounts (Tax-Advantaged)

| Account Type | Description |

|---|---|

| 401(k) | Employer-sponsored retirement plans |

| IRAs | Individual retirement accounts |

These offer tax advantages that can help your money grow faster.

Non-Retirement Accounts

| Account Type | Best For |

|---|---|

| Brokerage accounts | General investing |

| Education accounts | College savings |

| HSAs | Health Savings Accounts for medical expenses |

Diversifying your investment accounts can help manage the taxes you will have to pay over time, giving you more flexibility as your needs change.

Organizations like U.S. Bank and U.S. Wealth Management may offer various account options, though they may not directly offer insurance products but could refer you to an affiliated or third party insurance provider for products like annuities. Always check if providers are an Equal Housing Lender when applicable.

How to Actually Start Investing Your Money

When I began, I felt overwhelmed by all the research and decision-making involved in managing investments. Here are four approaches based on your situation:

Option 1: Micro-Investing Apps (Best for Complete Beginners)

If you are a complete beginner with small amounts to invest, micro-investing apps like Acorns and Stash make investing simple.

How they work:

- Round up your everyday purchases

- Invest the spare change for you

- Offer beginner-friendly educational resources and helpful tools

- Build your confidence gradually

📝 Note: U.S. Bank is not affiliated with these platforms. Also, monthly fees can eat into your returns if you are investing small amounts.

Option 2: Robo-Advisors (Best for Hands-Off Investors)

If you have a bit more money and prefer minimal involvement, consider a robo-advisor for hands-off investing.

Benefits:

- Share your goals, timeline, and risk tolerance

- The platform picks investments and handles monitoring

- Minimum deposits vary by provider

- Some offer access to a financial professional for added support

Option 3: Financial Professional (Best for Personalized Guidance)

For those ready to invest more and seeking personalized guidance, working directly with a financial professional means getting a custom investment plan tailored to your financial goals and risk tolerance.

Keep in mind: Advisors charge fees which may reduce your returns.

Option 4: Self-Directed Investing (Best for DIY Enthusiasts)

Want complete control? Self-directed investing lets you pick and manage your own investments.

Features:

- Usually no or low account minimums

- Access to tools and resources for decision-making

- Requires time to learn and research thoroughly

Maintaining Your Portfolio for Long-Term Wealth

Investing is rarely a set-it-and-forget-it activity. Your portfolio may need attention if:

- It requires further diversification

- Market changes occur significantly

- A major lifestyle shift justifies an adjustment to your portfolio

Building long-term wealth means staying engaged without overreacting to every headline.

Navigating Market Volatility and Economic Shifts

Market volatility is a fact of life. Investments can go down as well as up, and staying focused on the long haul is essential.

Getting Support During Uncertainty

A financial professional can be a helpful sounding board during rocky situations, offering a clear perspective and helping you understand your options.

Understanding Interest Rate Impact

Understanding how interest rates affect your financial life and investment portfolio is crucial:

| Factor | Relationship |

|---|---|

| Bonds vs Interest rates | Inverse relationship |

| When rates rise | Bond prices fall |

| Rising rates or falling rates | Trickle-down effect on stocks |

While interest rates do not directly affect stock prices, the ripple effects matter for your overall strategy.

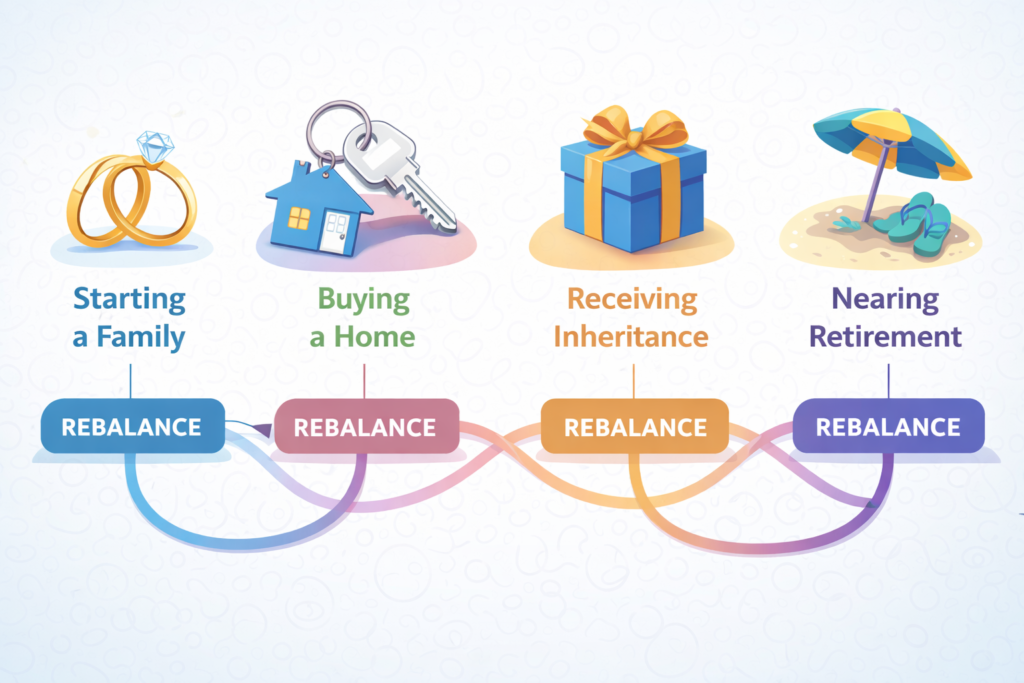

Adapting Your Strategy to Life Events

Even if you prefer being a hands-off investor, certain moments demand an active role in realigning assets. This is called rebalancing.

Life Events That Trigger Rebalancing

- 👶 Starting a family

- 🏠 Buying a house

- 💰 Receiving an inheritance

- 🎯 Nearing retirement

Each of these milestones shifts your priorities, and your investment strategy should shift accordingly to help you build wealth in alignment with your current reality.

Taking the Next Step with Confidence

Whether you choose investing online or prefer the guidance of a financial professional, the most important thing is to start.

Understanding asset classes like cash, bonds, real estate, and equities gives you the vocabulary to have informed conversations and make smart choices.

From my own experience, the hardest part was simply beginning—but once I did, I realized that growing money over time through compound growth was not some impossible feat reserved for experts. It was something I could do too, and so can you.

Frequently Asked Questions (FAQs)

How much money do I need to start investing?

You can start investing with as little as $5 using micro-investing apps like Acorns or Stash. These platforms round up your everyday purchases and invest your spare change automatically.

Is investing risky for beginners?

All investing involves risk, including the potential for loss or principal loss. However, a diversified long-term strategy with proper risk tolerance assessment can help manage these risks effectively.

What’s the difference between a 401(k) and an IRA?

A 401(k) is an employer-sponsored retirement plan, while an IRA (individual retirement account) is opened independently. Both offer tax advantages for retirement savings.

How does compound growth work?

Compound growth occurs when your investment returns generate their own returns. For example, if $1,000 earns 7% ($70), the next year you’re earning 7% on $1,070, creating accelerating wealth over time.

Should I pay off debt before investing?

Generally, yes. Tackle high-interest debt like credit card debt and personal loans first. Build an emergency fund covering three to six months of living expenses before you start investing.

Do I need a financial advisor to start investing?

No, but a financial professional can provide personalized guidance and create a custom investment plan. Robo-advisors offer a middle ground with lower fees and automated portfolio management.

📩 Ready to Start Your Investment Journey?

Take action today: Download a beginner-friendly micro-investing app, open your first brokerage account, or schedule a consultation with a financial professional. The sooner you start, the more time your money has to grow through the power of compound growth.

Have questions about investing with small amounts? Drop a comment below or share this guide with someone starting their wealth-building journey!

How Can I Advance My Career Without Changing Jobs in Libya: Complete Guide for 2026

Disclaimer

The information provided in this article is for educational purposes only and should not be considered tax or legal advice. Your financial situation is unique. Consult a tax advisor or legal advisor for advice concerning your particular situation. Investment products involve risk, including the possible loss of principal. Past performance does not guarantee future returns.

Founder of Jobzhandle.com | Career Strategist & Personal Finance Enthusiast. I help professionals grow their skills, manage their money wisely, and explore new income opportunities. My goal is to turn career and financial goals into reality with simple, proven tips.